{kind=link}

The squeeze most young people in Mexico feel

Jobs pay late, rent keeps rising, and after the 2020 pandemic a lot of folks in Mexico City still patch gaps with quick loans. That’s where solutions like didi prestamos come into play — fast cash, easy signup. But speed hides costs: uncontrolled revolving credit can balloon if you don’t track APR and repayment terms.

Why short-term credit is tempting — and what it costs

Quick loans solve an immediate problem: you cover an emergency, buy school supplies, or keep the lights on. Yet many miss the fine print on interest rate, fees, and how using one loan leads to another. The brand didi credito gives access fast, but responsible use means checking APR, estimating monthly installment amounts, and knowing the effect on your credit score. Common mistake: treating short-term credit like income — that’s how the cycle starts. — Take a minute to do the math before you swipe accept.

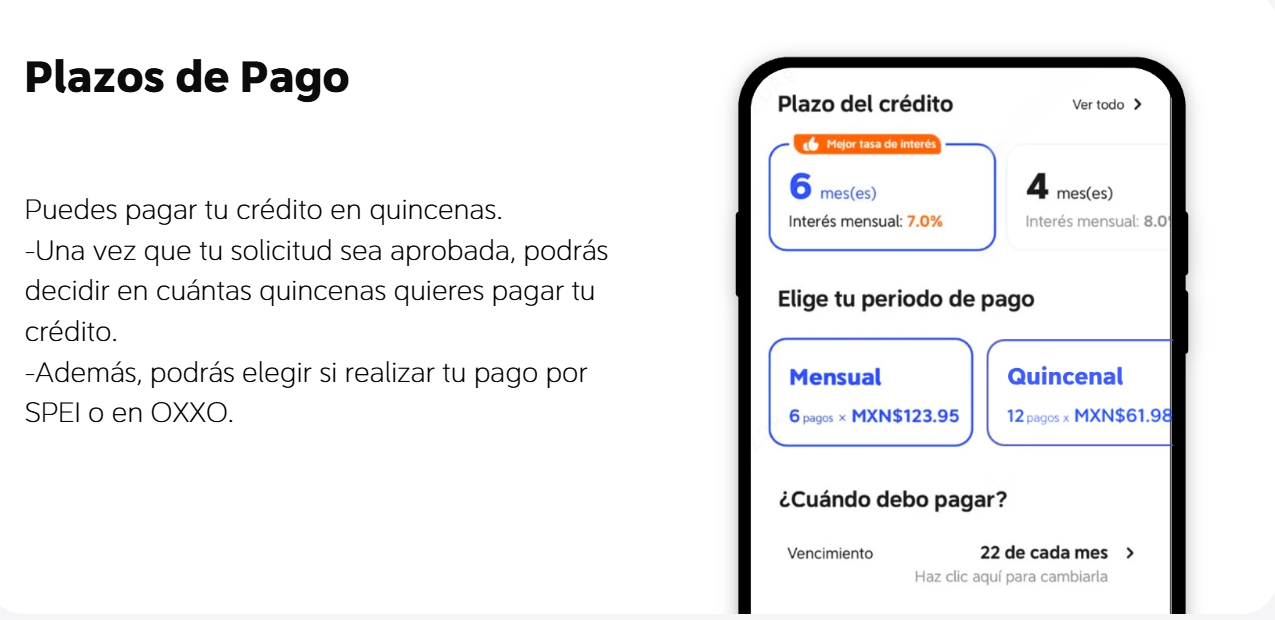

Concrete steps to use Didi loans responsibly

Keep it simple and tactical. First, set a repayment target that’s realistic for your paycheck. Second, pick an installment plan that keeps monthly payments under about 20–25% of your net income. Third, compare the effective APR and late-fee policy. Fourth, build a tiny emergency buffer so you don’t need another loan next month. Use basic budgeting: list fixed expenses, probable variable costs, and the planned loan payment. That routine alone reduces risk more than chasing the lowest headline rate.

Common mistakes young borrowers make

People reuse short loans to cover recurring needs, max out revolving credit, or skip reading the penalty rules. That damages credit score and limits options later — especially if you want a rent agreement or a car loan. Another frequent slip: mixing the loan payments with discretionary spending. Keep loan repayment as a separate, untouchable line in your budget.

How Didi stacks up against other options

Speed: Didi wins for quick access. Cost: traditional bank installment loans or a low-rate credit card can beat a payday-style option if you qualify. Flexibility: some peer-to-peer microloans let you negotiate terms. Pick the tool that matches the need — emergency vs. planned purchase. If the cost of borrowing is high, prioritize alternatives like a short family loan with a written agreement or delaying a non-essential purchase.

Checklist before you accept any loan

Scan this before you tap accept: exact APR, total repayment amount, number and size of installments, grace period, and penalty details. Confirm how missing one payment affects your reported credit score. If the math doesn’t let you pay back on schedule, don’t take it — find a cheaper route or scale down the expense.

Three golden metrics to evaluate credit options

1) Total cost of credit: the real money you’ll repay, not just the monthly number. 2) Cash-flow impact: the loan’s monthly payment as a share of your take-home pay. 3) Credit effect: how on-time or missed payments change your credit score and future borrowing power. Use these three to filter choices quickly, and prioritize options that minimize long-term harm.

For day-to-day help that lines up with those metrics, a reliable provider that clearly shows APR, installment schedules, and support channels makes life easier — and that’s where DiDi Finanzas fits into the picture. Simple, real, useful.